bymuratdeniz

Dear Partners and Friends,

Desert Lion Fund returned approximately -0.2% net for the month of October. Year to date, the Fund has returned +36.3% net, compared to the +14.9% returned by the JSE All Share Index (J203).

Early Xmas presents

The earnings of the companies in our portfolio continue to surprise to the upside. Recently, diversified home retailer Lewis Group (4.7% holding in the Fund) released a trading statement guiding that EPS is expected to increase by about 50% year-on-year. We await the earnings release and will report back in one of our upcoming letters.

Lewis is trading at around 7 times earnings and 0.8 times book. Throughout our South African opportunity set, we continue to see companies trading at single-digit PE’s despite growing at double-digit rates. Still in the early innings.

Fast and furious

Desert Lion specializes in finding mispriced opportunities in the relatively uncovered universe of SA small- and mid-caps. Over the past few years, that segment of the market suffered under the relentless strain of capital outflows and indiscriminate selling. Even if one was correct in one’s thesis about the fundamentals of a company, cheap just became cheaper as multiples contracted.

Consequently, our strategy struggled during the period 2021 to 2023.

That has changed.

As I have shared in recent letters, I believe we are in the early stages of a multi-year period of rewarding returns. The operating environment has decidedly changed for the better, the Desert Lion portfolio has never been in better shape, and our opportunity set is filled with high quality, high growth prospects that are trading at historically cheap valuations. When the market and global capital wake up to the latent returns in this relatively niche segment of global equities, the reaction will be fast and furious. Those who sleep in and wait for shouts of excitement to wake them up will miss more than half the move.

In the coming pages, I will illustrate why by way of a few charts and brief descriptions.

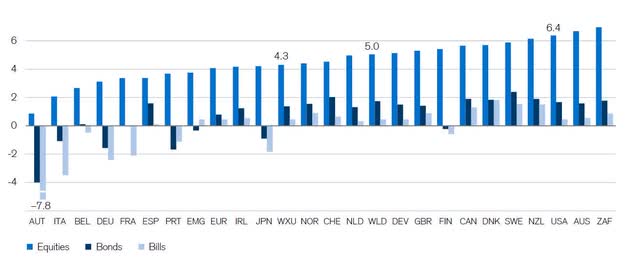

Despite recent underperformance, SA remains one of the best performing equity markets globally since 1900.

Source: Elroy Dimson, Paul Marsh and Mike Staunton, DMS Database 2023, Morningstar

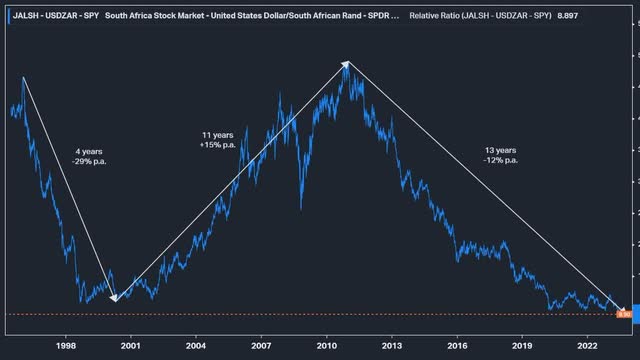

So, why doesn’t anyone want to own SA stocks? People take recent history and extrapolate it into the future… but people forget that markets move in cycles. The below chart illustrates the JSE (in USD) performance vs. S&P 500 (SP500, SPX) performance over the past 28 years. From 1996 to 2000, the JSE underperformed the S&P 500. Then tides changed and the JSE outperformed the S&P 500 for just over a decade from 2000 to 2011. However, from 2011 to 2023, the JSE underperformed the S&P 500. That trend has now reached an inflection point, whereby SA stocks have been outperforming the S&P 500 over the past several months. Market behavior will always allow for interim ups and downs, but, given the fundamental reasons for the shift, we believe this new trend will persist.

Source: Koyfin

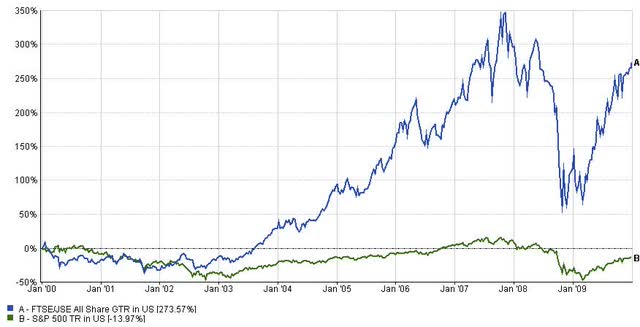

These inflection points result in trends that last several years. If you invested in the S&P 500 in 2000 and held that investment for a decade, your return would have been negative. However, had you invested in the JSE over the same decade, your return would be close to 274%. Yes, I know one can generate different charts over different periods that illustrate different outcomes. The point I am making is that, from a starting valuation perspective, current conditions are very similar to 2000.

Source: MWI, FE

We believe we are in the early stages of one of those inflection points that will result in a multiyear trend of rewarding performance from the JSE and especially the stocks we pick from our universe of JSE-listed small- and mid-caps. JSE stocks are the cheapest they have been in more than a decade.

Source: SBG Securities

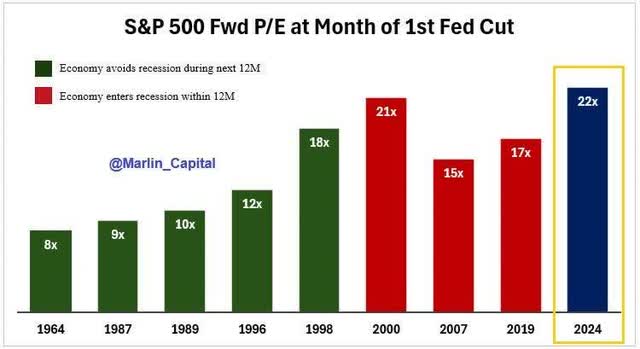

In contrast, US stocks are very expensive. We know what happened to JSE vs. S&P 500 returns in the decade following 2000. See the resemblance?

Source: @Marlin_Capital

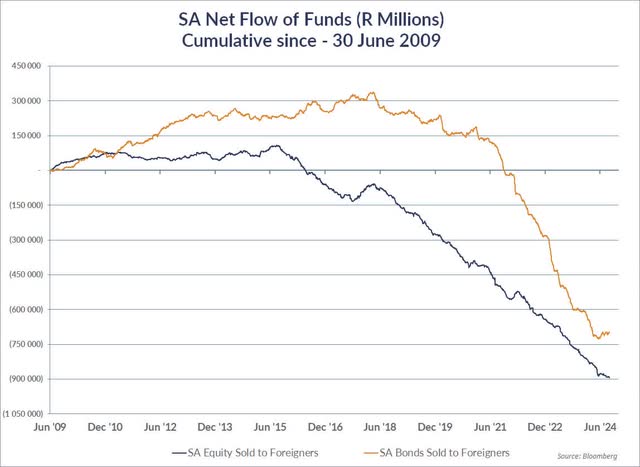

Not only are JSE stocks very cheap, they are extremely under-owned after years of capital outflows.

Source: MWI, Bloomberg

Source: SBG Securities

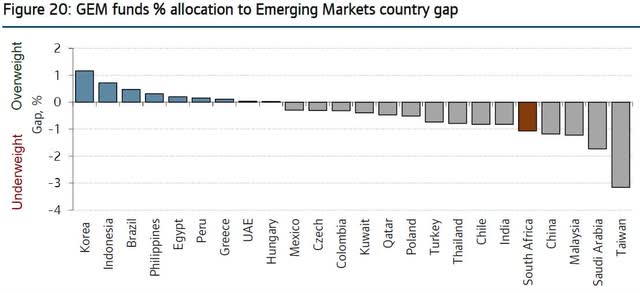

Global funds are underweight SA equities.

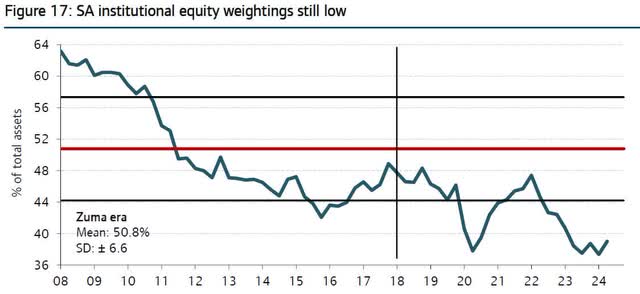

Local South African institutions are underweight SA equities.

Source: SBG Securities

In Closing

We are witnessing increased interest in the compelling set-up for SA equities. The political and economic outlook have improved dramatically. Inflation is under control and interest rates are decreasing. SA equities valuations relative to US equities valuations are at extreme cheap levels. However, we have not seen material capital inflows into the market yet. What happens when a local and global flood of liquidity tries to access a relatively small opportunity set? The reaction will be fast and furious.

Our portfolio is essentially fully invested in great companies with excellent prospects that are still trading at compelling valuations. We have an opportunity set, ready to invest in, that we believe should deliver several years of satisfactory returns.

To our limited partners, as always, I thank you for patiently entrusting Desert Lion with your hardearned capital. The majority of my wealth is invested in the Fund, right alongside yours.

All the best,

Rudi van Niekerk